Did you know that Agiblocks provides an integrated Value at Risk (VaR) engine that allows you to calculate your value at risk based on any selection of your business aspects – or even your entire portfolio – without the hassle of a complicated Monte Carlo simulation or other cumbersome computations? The information generated by our software can prove critical in your risk management activities and help you make decisions concerning your risk exposure, in real-time and wherever you need it.

The short version: in these volatile times especially, it is an essential – or indeed indispensable – tool in a CTRM solution that takes ‘RM’ just as serious as the CT-part. Please feel free to contact us for more information on the VaR module of Agiblocks. Or better yet: request a free demo of our Agiblocks CTRM Solution and step into the future!

Risk Management is 50 percent of your CTRM – literally

As with every investment in every sector, there are risks involved when trading commodities, even when it’s your actual business and not a portfolio strategy.

A big part of any CTRM system – about 50 percent, if we just count the R and M – has to do with dealing with risk. Commodity traders – as most other traders – tend to be risk averse: they prefer situations with low uncertainty over situations with high uncertainty.

Or better yet, no uncertainty at all.

It’s relatively easy to picture these risks when talking about mining and minerals like gold, steel and coal, or energy sectors like oil, gas and electricity. The agricultural sector too has its fair share of market risks though, whether it be in sectors like wheat, cotton and sugar, or related to coffee and cocoa beans. Luckily, risk can be managed – to a degree.

Value at Risk: what is it?

Value at risk (VaR) is a popular method for risk measurement. The indication of the level of risk you take with a certain investment can help you decide whether the possible gain is worth the potential maximum loss. It can be calculated for either one asset, a portfolio of multiple assets of an entire firm.

Value at Risk is a clear and comprehensible measure of the estimated risk of loss for any investment – ‘clear’ meaning fairly easy to use, and ‘estimated’ meaning there are no guarantees. In economics and finance, as well as in life, things are never one hundred percent certain, nor do the most certain outcomes yield the best results. However, understanding the possibilities of VaR in Agiblocks can make all the difference.

Value at Risk provides an estimation (or probability) of the size of the loss for an investment, given variables like asset size, market conditions and time constraints. For an investor, it’s all about probabilities, as the main focus of risk management is usually: ‘what are the odds of losing money?’. VaR is focused on that very presumption.

Calculating Value at Risk (VaR)

Calculating VaR answers the following question: ‘What can I, with a certain level of confidence, expect to lose in monetary or percentage terms, during a given period of time?’

VaR calculation consequently consists of three elements: a confidence level, a time period and the expected maximum loss. This could result in an answer resembling the following:

‘With 90 percent confidence, I expect my worst daily loss not to exceed 3.5 percent’.

1. Confidence

The first element is the level of confidence. This element represents the chance a certain risk may occur. Using the answer mentioned above, there is a 90 percent chance the worst daily loss will not exceed 3.5 percent. This element represents whether it is likely the maximum loss can be made and thus whether it is worth taking the risk.

2. Time constraint

The second element is the time constraint, the given horizon of the investment in terms of maturity. In other words, it represents the time period over which the loss can be realized. This can be expressed in daily, monthly or even yearly periods. This element is a factor for determining whether an investment represents a short- or long-term risk.

3. Expected maximum loss

The third and perhaps most important element is the expected maximum loss. This is indeed a crucial one, because it indicates what the worst-case scenario would be, should the risk become reality. This element must be considered before making an investment, to determine what this maximum loss may do to a trading account.

Furthermore, it can aid in making the decision whether the loss is acceptable considering the potential profit made on the investment.

Monte Carlo simulation

There are different methods for calculating VaR, including the historic method (which has become increasingly less used and relevant lately because of extreme market price volatility and increased amount of so-called Black Swan events in modern times), the Variance-Covariance method (which like the historic method does not require too big of a time investment but is likewise not the best way of incorporating off-market factors), and the aforementioned Monte Carlo approach, which uses simulations. A risk manager will perform a number of simulations, with each simulation using different input variables. These variables may range from level of volatility, initial price, correlation estimates, and so on.

All simulations will generate different outcomes which appear in a similar fashion to those of the other methods; a graph which shows the number each return is realized.

The advantage of using the Monte Carlo Method is that it will likely be more realistic compared to the other two methods. It also gives a risk manager the possibility to adjust his simulation to current market developments. This way their simulations can be more in sync with current market movements. It also gives the risk manager the opportunity to let his personal judgment be a factor for determining the probability at which a return may occur.

The Monte Carlo method however requires a lot of time and work to successfully be used in risk assessment. Moreover, with the number of factors influencing the returns, the number and complexity of the simulations must increase in order to simulate as many possible outcomes to get a reasonable estimate of the returns.

Value at Risk in Agiblocks

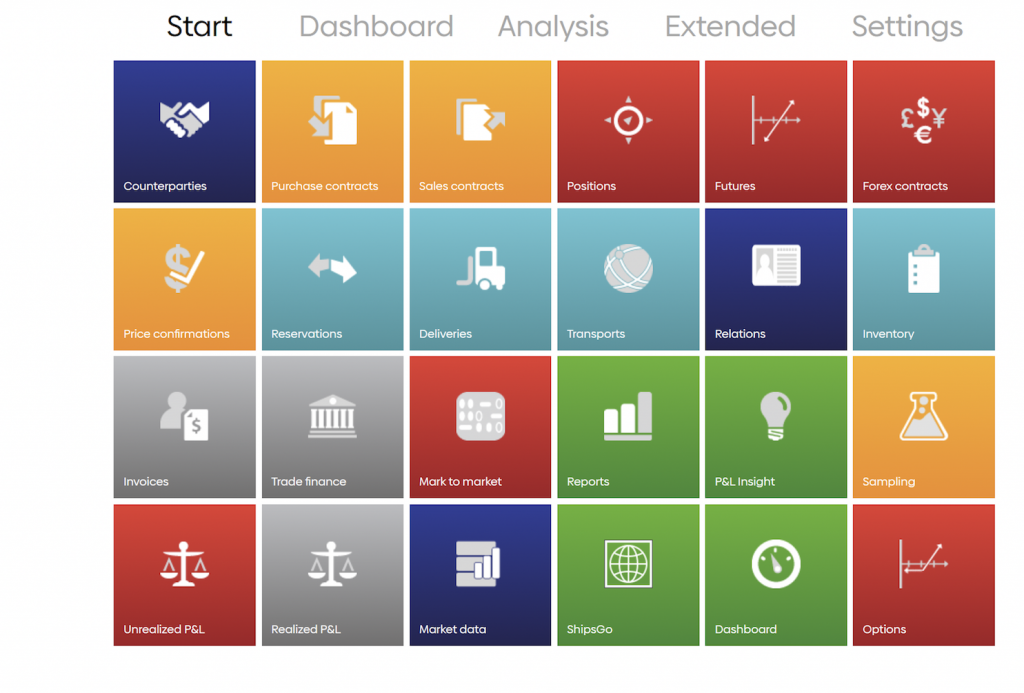

Agiblocks is a one-stop CTRM software solution designed by trade professionals, for trade professionals. To simply and streamline your fixed routine, it focuses on all the aspects of the daily practices of the trade. That means we focus on risk management too, with some great tools for markets analysis – such as our features for OTC contracts and What-If analysis. Here, we’d like to focus on our prowess in VaR (or Value at Risk, not to be confused with Video Assisted Referee, a totally different type of risk management) and how you can use the Agiblocks module on VaR as an insightful risk assessment tool.

As we’ve said before, the commodity trade is a volatile business even in the best of times. Risk management is a continuous loop that takes the route of risk identification, assessment, analysis and reporting to establishing key changes, communication and adaptation – and then back to risk identification. Defining those risks is key, so a dynamic margin management – keeping track of your position and changing course if needed – is an essential part of risk management analytics when dealing with predictability and profitability. That’s why we feature strong tools for risk management in Agiblocks.

Tools that have a valuable part to play in navigating these waters and weathering a storm for which there really are no reliable long-term forecasts.

In fact, we were talking to the team of one of our new clients the other week, who wish to do extensive risk assessments on every trade. Typically, that would (or could) involve the Monte Carlo approach (more on that in a little bit), but that requires a lot of data, and a lot of calculations. The team – and most teams, really – would then run these simulations outside of the system, because they either don’t have it in their CTRM solution of choice, or they don’t know they have it – in Agiblocks. Regarding the latter parties: they do the trade execution, the logistics, all the attributes, but they don’t really lean on their CTRM software for the RM-part of the solution. In other words, they’re missing out.

Agiblocks provides an integrated Value at Risk (VaR) module, which can calculate your value at risk based on your entire portfolio or a selection of your portfolio. The information generated by this module can prove critical in your risk management activities and help you make decisions concerning your risk exposure.

For more information on the VaR module of Agiblocks, please contact us directly or request a demo to take full advantage of all Agiblocks has to offer, without any obligation.

Risk and Position Management

Position management – and more specifically, real-time adjustments –can heavily influence ROI and is therefore a subject that deserves attention when talking about VaR (it’s discussed at length here, if you’re interested it reading more about risk management strategies).

Position management is all about quantities and timing. Agiblocks provides real-time position management and shows you whether you are long or short on a certain quality for a specific period in time. The quality is important, as not all your commodities are exchangeable. For example, you can be long on fair-fermented cocoa beans from Ghana and short on well-fermented cocoa beans from Ecuador; you cannot replace one with the other.

That is why Agiblocks offers ‘position hooks’, a category defined by quality properties visible in a certain time period. All equal qualities for a period are automatically calculated to one position number. In Agiblocks, you can dive into all underlying contracts and deliveries which will show you the build-up of that particular position. Moreover, the futures position is also visible, informing you immediately if you are properly hedged – or not.

Agiblocks offers:

- VaR, OTC contracting and What If Analysis

- Multiple entities & intercompany trade, multiple trade books

- Physical contract management for bulk, break bulk, containers, parcels

- Flexible position management (origins, specifications, premiums, certifications)

- Mark to Market valuation by position/parities/premiums and cost

- Hedging & derivative management (futures, options, OTC, forex)

- Cross markets (futures/forex) and/or ratio pricing, hedging, hedge allocation

- Logistic management (documentation & freight), physical inventories, sampling

- Financing & collaterals, invoicing, cost accruals, profit & loss: unrealized / realized

- Flexible reporting, document management, quality and trading dashboards

- General Accounting API, IFRS 15 & IFRS 9 compliant

But wait, there’s more! Our VaR Engine is fully equipped to handle all the information you have within Agiblocks, but there are ways to gather even more input – as you can find out in our feature on Agiblocks 4.0. In the catalog-section of our software, under Tools, you can find two new gems of unrivaled functionality: Link and External. Both allow using external content within the Agiblocks dashboard. Link opens a new tab for a specified link, while External page allows you to embed content. That means you can now import external reports while still working in your customized Agiblocks environment – something that could prove vital for your on-the-go risk assessments and subsequent adjustments.

Moreover, it opens up space for third parties to add their products to the system. It might very well lead to an interesting “market place” for parties to get involved and jointly add product improvements. Down the line, something like an Agiboo Store, an in-app boutique for products and services might very well be a reality. It could introduce purchases on subscription basis or as one-off fees, in-app, allowing you to further optimize and customize your dashboard with external content.

It’s how we’ve always envisioned the full potential of our flagship CTRM software.